Learn how to create a UPI ID, its format, benefits, and how to use it for seamless digital payments in India.

Digital payments in India have evolved rapidly, and the Unified Payments Interface (UPI) plays a central role in enabling instant money transfers. At the heart of this system is the UPI ID, which simplifies payments without requiring bank account details.

Understanding what a UPI ID is and how to create one allows users to access fast, secure, and convenient digital transactions.

What is a UPI ID?

A UPI ID, also known as a Virtual Payment Address (VPA), is a unique identifier linked to your bank account. It allows you to send and receive money without sharing sensitive details like account numbers or IFSC codes.

UPI ID Format

The typical format looks like:

username@bankname

Examples:

yourname@ybl

9876543210@paytm

yourname@okicici

The first part can be your name or mobile number, while the suffix represents your bank or payment provider.

Benefits of Using a UPI ID

UPI IDs are widely used in India due to their convenience and security.

Key Advantages

Secure Transactions: No need to share bank details; payments require a UPI PIN

Instant Transfers: Money is transferred in real time within seconds

24/7 Availability: Works anytime, including weekends and holidays

Low or No Charges: Most transactions are free

No Minimum Limit: Even ₹1 transactions are supported

Multiple Accounts: Link multiple bank accounts in one app

Offline Access: Use *99# for transactions without internet

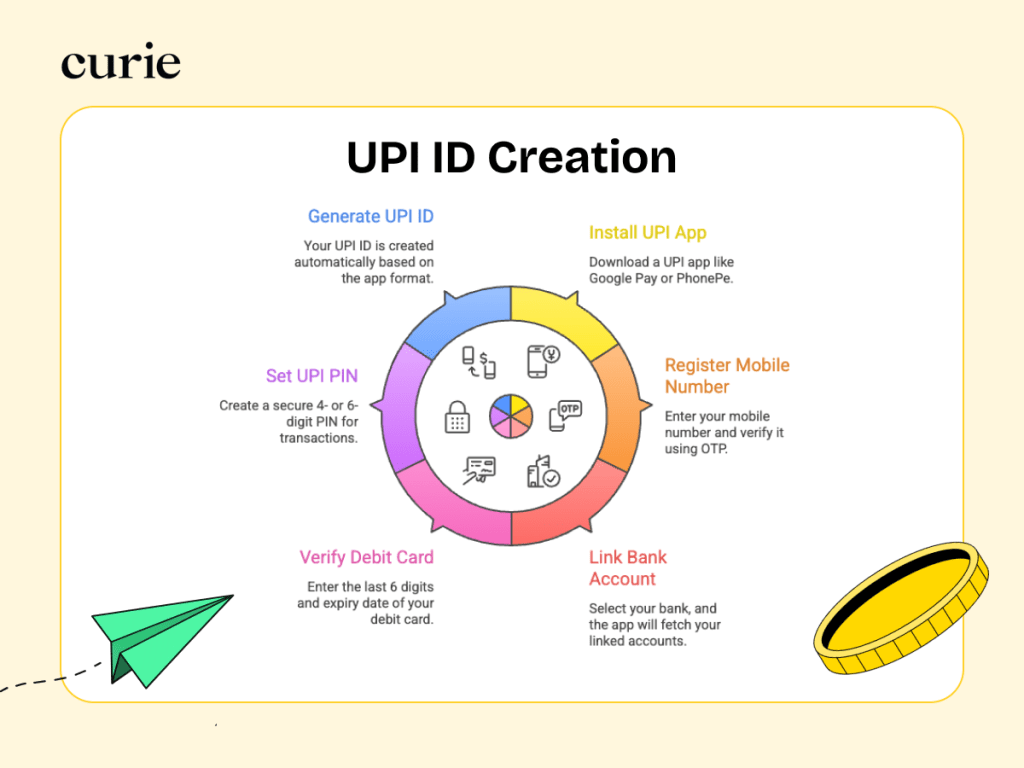

How to Create a UPI ID

Creating a UPI ID is simple and takes only a few minutes.

Download apps like Google Pay, Curie Money UPI, PhonePe, Paytm, or BHIM.

Step 2: Register Mobile Number

Enter your mobile number and verify it using OTP.

Step 3: Link Bank Account

Select your bank; the app fetches linked accounts automatically

Step 4: Verify Debit Card

Enter the last 6 digits and expiry date of your debit card.

Step 5: Set UPI PIN

Create a secure 4- or 6-digit PIN for transactions.

Step 6: Generate UPI ID

Your UPI ID is created automatically based on the app format.

How to Create UPI ID Without Internet

Users without smartphones can still access UPI services:

Dial *99#

Select your bank

Enter debit card details

Set UPI PIN

This allows basic services like sending money and checking balance.

How to Use a UPI ID for Payments

Sending money using a UPI ID is straightforward:

Open your UPI app

Select Send Money

Enter recipient UPI ID

Enter amount

Confirm using UPI PIN

The transaction is completed instantly.

UPI Security Tips

Never share your UPI PIN or OTP

Always verify recipient details

Use trusted apps only

Avoid unknown QR codes or links

Enable app lock or biometric security

Conclusion

A UPI ID simplifies digital payments by eliminating the need for bank details while ensuring secure and instant transactions. With easy setup and widespread acceptance, UPI has become an essential part of India’s financial ecosystem. Creating a UPI ID takes only a few minutes and enables seamless money transfers anytime, anywhere.

FAQs

1. Can I create multiple UPI IDs?

Yes, multiple UPI IDs can be created for the same bank account.

2. Is sharing a UPI ID safe?

Yes, it only allows receiving money, not withdrawals.

3. What if I forget my UPI PIN?

Reset it using the “Forgot UPI PIN” option.

4. Are UPI transactions free?

Most peer-to-peer transactions are free.

5. What is the UPI transaction limit?

Typically ₹1,00,000 per transaction, depending on the bank.

Understanding LTCG tax is essential for maximizing post-tax returns. Union Budget 2024 brought significant changes effective July 23, 2024. This guide explains current tax rates, calculations, and planning strategies.

What is Long-Term Capital Gains?

Long-term capital gains represent profit from selling a capital asset after holding it beyond a specified minimum period. For mutual funds, whether gains qualify as long-term depends on fund type and holding duration.

Formula: Capital Gain = Sale Value (Redemption NAV × Units) – Purchase Cost (Purchase NAV × Units) – Expenses

If held beyond the minimum period, it’s LTCG; otherwise, it’s short-term capital gains (STCG), taxed differently.

Holding Period Requirements

Equity-Oriented Funds (65%+ equity)

– LTCG: Holding period more than 12 months

– STCG: Holding period 12 months or less

Includes equity funds, ELSS, hybrid equity funds, equity index funds.

Debt-Oriented Funds

Taxation rules changed fundamentally from April 1, 2023:

– Investments on/after April 1, 2023: All gains taxed at income tax slab rate (any holding period)

– Investments before April 1, 2023: Rules vary by sale date (see table below)

Includes debt funds, liquid funds, gilt funds, banking & PSU funds.

Current LTCG Tax Rates (Post-Budget 2024)

Equity Funds (Holding > 12 months)

Tax Rate: 12.5% (no indexation)

Annual Exemption: ₹1.25 lakh per financial year (cumulative across all equity funds, shares, and equity instruments)

Budget 2024 Changes

Category

Previous

Current

Tax Rate

10%

12.5%

Exemption Limit

₹1 lakh

₹1.25 lakh

Debt Funds – Timeline Table

Investment Date

Sale Date

Holding Period

Tax Treatment

On/after Apr 1, 2023

Any date

Any period

Income tax slab rate

Before Apr 1, 2023

On/after July 23, 2024

> 24 months

12.5% (no indexation)

Before Apr 1, 2023

On/after July 23, 2024

≤ 24 months

Income tax slab rate

Before Apr 1, 2023

Before July 23, 2024

> 36 months

20% (with indexation)

Before Apr 1, 2023

Before July 23, 2024

≤ 36 months

Income tax slab rate

Understanding Indexation (Now Removed)

Indexation adjusted purchase cost for inflation using the Cost Inflation Index (CII), reducing taxable gains.

Budget 2024 removed indexation for most assets sold after July 23, 2024.

Calculating LTCG Tax: Examples

Example 1: Equity Fund – No Tax (Below Exemption)

Investment: ₹2,00,000 in January 2023

Redemption: ₹2,50,000 in March 2025 (26 months holding)

Step 1: Calculate gain

Gain = ₹2,50,000 – ₹2,00,000 = ₹50,000

Step 2: Check holding period

26 months > 12 months = LTCG ✓

Step 3: Apply exemption

₹50,000 < ₹1.25 lakh exemption

Tax payable: ₹0

Example 2: Equity Fund – With Tax (Above Exemption)

Investment: ₹5,00,000 in June 2022

Redemption: ₹7,00,000 in September 2024 (27 months)

Gain: ₹2,00,000

Calculation:

– Exempt amount: ₹1,25,000

– Taxable gain: ₹2,00,000 – ₹1,25,000 = ₹75,000

– Tax: ₹75,000 × 12.5% = ₹9,375

(Plus 4% cess = ₹9,750 total)

SIP Investments: Separate Taxation

Each SIP installment is treated as a separate investment with its own holding period.

Example:

SIP: ₹10,000 monthly starting January 2023

Full redemption: March 2025

Tax treatment:

– January 2023 SIP: Held 26 months = LTCG

– February 2023 SIP: Held 25 months = LTCG

– March 2024 SIP: Held 12 months = STCG (exactly 12 months qualifies as short-term)

– April 2024 onwards: All STCG

Result: Mixed LTCG and STCG. Fund house provides detailed breakup for tax filing.

Planning tip: Redeem after all installments cross 12 months to maximize LTCG benefits.

Tax-Saving Opportunities

ELSS (Equity Linked Savings Scheme)

– Benefit: Section 80C deduction up to ₹1.5 lakh on investment (old tax regime only)

– Lock-in: 3 years mandatory

– LTCG on redemption: Taxed like regular equity funds (12.5% above ₹1.25 lakh)

Important: ELSS provides tax deduction on investment, not exemption on gains.

Section 54EC (Capital Gains Bonds)

– Invest LTCG in specified bonds (NHAI/REC) up to ₹50 lakh within 6 months

– Entire invested LTCG gets tax exemption

– Lock-in: 5 years, Returns: ~5-5.5%

Works only for large gains where you can lock money for 5 years.

Filing Requirements

ITR Form: ITR-2 (ITR-1 doesn’t allow capital gains)

Schedule: Schedule CG (Capital Gains)

Requirements:

– Transaction statements from fund house/platform

– Purchase and redemption dates with NAV

– Calculate STCG and LTCG separately

– Report all gains (even below exemption)

Record keeping: Maintain statements for at least 6 years.

Budget 2024 Changes Summary

Budget 2024 – Equity & Debt Tax Changes

Aspect

Before (till July 22, 2024)

After (from July 23, 2024)

Equity LTCG Rate

10%

12.5%

Equity Exemption

₹1 lakh/year

₹1.25 lakh/year

Indexation

Available (debt pre-Apr 2023)

Removed

Debt Holding Period

36 months

24 months (pre-Apr 2023 only)

Net impact: Higher exemption offsets rate increase for moderate gains (₹1-1.5 lakh). Larger gains pay slightly more tax.

Smart Redemption Planning

1. Wait for LTCG Qualification

If near the 12-month mark, wait to qualify for 12.5% LTCG instead of 20% STCG.

2. Spread Across Financial Years

₹3 lakh gains? Redeem ₹1.25 lakh in FY 2024-25, ₹1.75 lakh in FY 2025-26. Saves ₹15,625 in taxes.

3. Use Family Exemptions

Each family member gets separate ₹1.25 lakh exemption. Consider investments in spouse/children’s names (with their PAN/KYC).

4. Offset with Losses

Losses in other equity investments can offset LTCG from mutual funds, reducing taxable gains.

5. Track Total Portfolio

Monitor cumulative gains across all equity investments (funds + stocks) to plan within exemption limits.

Key Takeaways

✓ Equity funds: Hold >12 months, pay 12.5% tax on gains above ₹1.25 lakh annual exemption

✓ Debt funds: Investments after April 1, 2023 taxed at slab rate regardless of holding period

✓ Indexation removed: For most assets sold after July 23, 2024

✓ SIPs: Each installment taxed separately based on its holding period

✓ ELSS: Provides investment deduction (Section 80C), not gains exemption

✓ Annual exemption: ₹1.25 lakh is cumulative across all equity investments per financial year

✓ Tax planning: Strategic redemption timing can save significant taxes

Conclusion

While tax efficiency matters, prioritize financial goals, risk tolerance, and investment horizon first. Tax considerations should inform redemption timing, not whether you invest.

Stay updated on tax law changes, maintain proper records, and consult qualified tax professionals for complex situations involving multiple transactions or large gains.

Curie Money (AMFI ARN: 257706) partners with ICICI Prudential and Bajaj Finserv for transparent investment solutions. For specific tax guidance, always consult a qualified chartered accountant or tax consultant.

Disclaimer:

Mutual fund investments are subject to market risks. Read all scheme-related documents carefully. This information is for educational purposes only, not tax advice. Tax laws are subject to change and individual circumstances vary. Always consult a qualified tax professional for personalized guidance.

Liquid funds offer better returns than savings accounts with near-instant accessibility, making them ideal for parking surplus cash or building an emergency fund.

Understanding Liquid Funds

Liquid funds are debt mutual funds that invest exclusively in ultra-short-term money market instruments with maturities of up to 91 days. These include treasury bills, commercial papers, certificates of deposit (CDs), and short-term government securities.

The primary objective is to preserve capital while generating reasonable returns with high liquidity. Think of liquid funds as a smart alternative to keeping large amounts in your savings account – you earn better returns while maintaining quick access to your money.

What Do Liquid Funds Invest In?

Treasury Bills (T-Bills): Government-issued securities maturing in 91 days or less. These carry zero credit risk since they’re backed by the government.

Commercial Papers (CPs): Short-term unsecured promissory notes issued by highly-rated corporations (typically A1+ rated) to meet working capital needs. Maturity: 7-90 days.

Certificates of Deposit (CDs): Time deposits issued by banks with maturities of 7-90 days, offering slightly higher rates than savings accounts.

Repo/Reverse Repo: Short-term lending/borrowing agreements backed by government securities, typically overnight to 14 days.

Call Money: Ultra-short-term lending between banks, usually overnight.

All instruments are high-quality (rated A1+ or equivalent) to minimize credit risk. The portfolio is diversified across multiple issuers to spread risk.

How Liquid Funds Work

Fund managers create a professionally managed pool that invests in these short-term instruments. Since securities mature within days or weeks, the portfolio is constantly refreshed with new investments.

NAV Calculation: Unlike other mutual funds that use previous day’s closing prices, liquid funds use a unique system – NAV is based on the average of the last 30 days (for investments) or 90 days (for redemptions). This reduces volatility and prevents market timing by large investors.

Return Generation: Liquid funds generate returns purely from interest income earned on underlying instruments. There’s minimal capital appreciation since bonds are held until maturity. Returns are predictable and stable, not explosive like equity funds.

Example: If you invest ₹1 lakh in a liquid fund offering 5% annual returns:

– 1 month: ~₹417 (approximately)

– 3 months: ~₹1,250

– 6 months: ~₹2,500

– 1 year: ~₹5,000

Compare this to a savings account at 3% annual interest:

– 1 year on ₹1 lakh: ~₹3,000

Extra earnings: ₹2,000 annually with similar liquidity.

Key Features

No Lock-in Period: You can redeem your investment anytime. Regular redemptions are processed within 1 business day (T+1 settlement).

Instant Redemption Facility: Most liquid funds offer instant redemptions up to ₹50,000 or 90% of your investment (whichever is lower) directly to your bank account within minutes. This facility is available 24/7, including weekends and holidays.

Minimal Charges: No entry load. Exit load is minimal – typically 0.0070% per day if you redeem within 7 days. For example, redeeming ₹1 lakh after 3 days incurs just ₹21 exit load.

Low Interest Rate Risk: Since securities mature within 91 days, liquid funds are barely affected by interest rate changes. Even if RBI raises rates, your existing holdings mature quickly and get reinvested at new, higher rates.

Flexible Investment Amounts: Start with as low as ₹5,000 or invest ₹5 lakh+ depending on your surplus cash needs.

Liquid Funds vs. Alternatives

Feature

Liquid Funds

Savings Account

Fixed Deposits

Overnight Funds

Returns

4-6% annually

3-4% annually

6-7% annually

3.5-4.5% annually

Liquidity

24 hours (instant up to ₹50k)

Instant

Penalty on early withdrawal

24 hours

Risk

Very Low

Minimal

Very Low (DICGC insured)

Ultra Low

Lock-in

None

None

Fixed tenure

None

Tax Efficiency

Better (indexation after 3yrs)

Interest fully taxable

Interest fully taxable

Similar to liquid

Best For

Emergency fund, short-term parking

Daily transactions

Fixed goals 1-5 years

Ultra-conservative

Key insight: Liquid funds offer the best balance between returns and accessibility for money you need in 1-6 months.

Benefits of Liquid Funds

Better Returns Than Savings Accounts: Earn 4-6% annually compared to 3-4% in savings accounts – that’s 50-100% higher returns on your idle cash.

Quick Accessibility: Regular redemptions settle within 1 business day. Instant redemption up to ₹50,000 available within minutes through most platforms.

Lowest Risk in Mutual Funds: Liquid funds are the safest mutual fund category due to high-quality, ultra-short-duration investments. Default risk is minimal given stringent credit rating requirements.

Tax Efficiency: More tax-efficient than savings account or FD interest, especially if held for 3+ years (explained below).

No Penalties: Unlike fixed deposits, you can withdraw anytime without penalty (except tiny exit load within 7 days).

Who Should Invest in Liquid Funds?

Emergency Fund Builders: If you’re building a 3-6 month emergency corpus, liquid funds offer better returns than savings accounts while maintaining accessibility.

Short-Term Goal Savers: Saving for a vacation in 6 months? Down payment in 1 year? Park funds here until needed.

Between Investments: Received a bonus or sold property? Park money temporarily in liquid funds while researching long-term investment options.

Business Working Capital: Entrepreneurs managing cash flows can earn better returns on business reserves without compromising accessibility.

Conservative Investors: Risk-averse individuals wanting slightly better returns than bank deposits with minimal risk.

Tax Treatment of Liquid Funds

Liquid funds follow debt fund taxation rules:

Short-Term Capital Gains (holding < 3 years):

Added to your annual income and taxed at your income tax slab rate.

Example: You earn ₹10,000 profit after 6 months. If you’re in the 30% tax bracket, you pay ₹3,000 tax (plus cess).

Long-Term Capital Gains (holding ≥ 3 years):

Taxed at 20% with indexation benefit, which adjusts your purchase price for inflation.

Example: Invest ₹2,00,000 for 3.5 years, redeem at ₹2,40,000 (₹40,000 gain). With indexation, your taxable gain might reduce to ₹20,000, so you pay just ₹4,000 tax instead of ₹8,000.

Reality check: Most people use liquid funds for under 1 year, so STCG taxation applies. Still, even after taxes, returns beat savings accounts.

Risks to Consider

Credit Risk: While minimal due to high credit ratings, there’s a small risk that an issuer (corporate) could default on commercial paper. However, this is rare given strict rating requirements.

Interest Rate Risk: Though minimal due to short duration, sudden sharp rate increases can cause minor NAV fluctuations of 0.1-0.3%.

Inflation Risk: At 4-6% returns, liquid funds barely keep pace with inflation (5-6% typically). They preserve purchasing power but don’t significantly grow wealth.

Not DICGC Insured: Unlike savings accounts (insured up to ₹5 lakh), liquid funds are market-linked investments without deposit insurance.

Expected Returns: Reality Check

Historical performance: 4-6% annually over 5-10 year periods

Current scenario (2025): With repo rate around 6-6.5%, liquid funds offer approximately 5-6%

Best-case scenario: 7-8% during high interest rate environments

Worst-case scenario: 3-4% during low rate environments

Important: Liquid funds won’t make you rich. Their purpose is capital preservation with slightly better returns than savings accounts, not wealth creation.

Decision Framework: Should You Invest?

Invest in liquid funds if:

– You need money within 1-12 months

– You want better returns than savings accounts with low risk

– You’re building an emergency fund

– You need high liquidity without penalties

– You have surplus cash earning just 3-4% in savings

– You may park your money with Curie Money which is subsequently parked in liquid funds, and as and when you require the money, the funds are liquidated

How to Choose the Right Liquid Fund

When selecting a liquid fund, evaluate:

Historical Returns: Compare 1-month, 3-month, and 1-year returns across similar funds. Consistency matters more than occasional outperformance.

Expense Ratio: Lower is better. Direct plans should have expense ratios below 0.25%; regular plans below 0.50%.

Credit Quality: Check portfolio composition – prefer funds with 80%+ in AAA/A1+ rated instruments and government securities.

AUM Size: Larger funds (₹1,000+ crore) typically offer better liquidity and stability.

Fund House Reputation: Established AMCs with strong debt fund track records are preferable.

Instant Redemption: Verify the fund offers instant redemption facility up to ₹50,000.

No effort investing: You may choose to park your money with Curie Money and they take care of choosing the right liquid fund! Whenever you need your money, the investment is liquidated instantaneously!

Bottom Line

Liquid funds are the reliable, sensible choice for short-term money management – offering accessibility, stability, and better returns than savings accounts. They won’t create wealth, but they’ll preserve it while earning reasonable returns.

Every investor should have liquid funds in their financial toolkit for emergency funds, short-term goals, or temporary cash parking. They’re the bridge between savings accounts and longer-term investments.

Disclaimer:

Mutual fund investments are subject to market risks. Read all scheme-related documents carefully before investing. Past performance doesn’t indicate future results. Liquid funds carry credit risk and interest rate risk, though minimal compared to other debt funds.

Curie Money (AMFI ARN: 257706) partners with YES Bank, ICICI Prudential, and Bajaj Finserv to offer trusted investment solutions including liquid funds with instant redemption facilities.

This choice can impact your long-term wealth by lakhs of rupees. This guide explains the differences, cost implications, and which suits your situation.

What Are Direct and Regular Plans?

Same fund, different distribution channels – like buying from the manufacturer vs. retail store.

Regular Plans: Via intermediaries (distributors, advisors, banks, brokers). AMC pays them commissions (built into expense ratio). They help with fund selection, paperwork, advice, transactions, reviews. Companies such as Curie Money offer fantastic regular mutual funds (more specifically Liquid Funds) which can be liquidated almost instantaneously. The way it works is that you can park your money (cash) in Curie Money and Curie chooses the most suited fund where the investor can make short term returns! As and when you choose to withdraw the money, the fund will be liquidated instantaneously!

Direct Plans: Directly from AMC (website, app, offices) or RTA platforms (CAMS, Karvy). No intermediary = no commission = lower expense ratio.

Impact Example: Rs. 10K monthly SIP for 20 years at 12% gross returns:

– Direct (1% expense): ₹89.73L

– Regular (2% expense): ₹76.57L

– Difference: ₹13.16L

1% expense difference = ₹13L+ loss due to compounding!

Higher NAV in Direct Plans

Lower expense ratio → faster NAV growth. Same fund, portfolio, manager – different outcomes.

Example: Starting NAV ₹10, 12% gross return:

– After 1yr: Direct ₹11.10 (11% net), Regular ₹11.00 (10% net)

– After 10yrs: Direct ₹28.39, Regular ₹25.94

Direct vs Regular: Detailed Comparison

Aspect

Direct Plan

Regular Plan

Expense Ratio

Lower (0.5-1% lower)

Higher (includes distributor commission)

NAV

Higher over time due to lower expenses

Lower over time due to the commission charges

Returns

Higher (since more of the return stays with you)

Lower (due to commission and distribution fees)

Investment Method

Directly from AMC or through direct platforms

Through intermediaries (distributors/advisors)

Guidance

Self-directed or with fee-based advisors

Guidance provided by distributors/advisors

Paperwork

You handle or platform assists

Distributor handles paperwork

Cost of Advice

Separate (if using a fee-based advisor)

Included in the expense ratio (through commissions)

Transparency

High (costs and fees are transparent)

Lower (commission is included in the expense ratio)

Best For

DIY investors, informed investors

Investors seeking advice or guidance

Direct Plans Advantages

Higher returns over time, full transparency, cost efficiency, same fund/manager at lower cost, better for long-term goals, digital convenience.

Regular Plans Advantages

Professional guidance, behavioral coaching during downturns, comprehensive financial planning, convenience (paperwork handled), handholding for elderly/tech-uncomfortable, periodic reviews/rebalancing.

Fee-Based Advisory (Middle Ground)

Invest in direct plans while working with SEBI-Registered Investment Advisor (RIA).

RIAs: Transparent fee, unbiased advice, legally fiduciary. Pay RIA separately + invest in direct plans.

Cost Example: Direct 1% + RIA 0.5% = 1.5% total vs. Regular 2% = Save 0.5% with professional advice!

Which to Choose?

Direct: Comfortable researching/selecting funds, understand investment concepts, have time/interest, digitally savvy, want to minimize costs, can maintain discipline, willing to self-educate.

Regular: New to investing, no time/inclination for research, value advisor relationship, need broader planning (insurance, tax, estate), willing to pay for convenience, need emotional decision prevention, uncomfortable with technology. Curie Money offers investment into liquid funds using your idle funds, to help make returns while you’re not using your money!

Fee-Based (Direct + RIA): Want professional advice with cost efficiency, value transparency, want fiduciary advice, willing to pay separately, have reasonable portfolio size.

Misconceptions Debunked

Myth 1: “Regular = better service” → Reality: Service quality depends on individual distributor, not plan type.

Myth 2: “Direct = risky, no guidance” → Reality: Fund is identical; risk doesn’t change.

Myth 3: “Difference too small” → Reality: 1% over 20 years = lakhs lost to compounding.

Myth 4: “Need expertise for direct” → Reality: Basic education sufficient for diversified funds.

Myth 5: “Commission advisors = bad advice” → Reality: Many ethical, but structure creates conflicts vs. fee-based.

Decision Framework: Which Plan Type Suits You?

1. Knowledge & ConfidenceDo you understand fund categories, risk tolerance, and diversification? Can you evaluate funds independently?

2. Time & InterestAre you willing to research funds, stay updated on market trends, and review your portfolio periodically?

3. Emotional DisciplineCan you stick to your investment plan during market crashes and avoid impulsive decisions based on short-term volatility?

4. Technology ComfortAre you comfortable using investment apps, completing online KYC, and managing digital transactions independently?

5. Cost SensitivityDo you have a portfolio size (₹5+ lakh) where saving 0.5-1% annually translates to meaningful long-term savings?

Mostly “Yes” answers: Direct plans are ideal for you Mostly “No” answers: Regular plans with a trusted advisor may be more appropriate

Tips

Direct: Educate yourself (SEBI, AMC sites), start simple (index funds), use SIP, review annually, stick to plan, diversify.

Yes, but treated as redemption + fresh purchase → capital gains tax + holding period resets.

When: Equity funds >12 months with gains <Rs. 1.25L = minimal tax. Debt funds less efficient.

Alternative: Future = direct; existing regular = continue till maturity.

Long-Term Perspective

Starting to invest > perfect plan selection. Asset allocation matters more. Stay invested through cycles. SIPs build wealth regardless of plan. Goals should drive decisions, not just cost.

Conclusion

No universal answer. Depends on knowledge, confidence, time, and guidance needs.

Value is subjective: If guidance helps you choose appropriate funds, maintain discipline, avoid mistakes, plan comprehensively – regular/fee-based advisory may be worthwhile.

Make informed choices, not defaults. Curie Money (AMFI ARN: 257706) offers knowledge and transparent options.

Disclaimer:

Mutual fund investments subject to market risks. Read all documents carefully. Past performance doesn’t indicate future results. Choice based on individual circumstances, knowledge, comfort. Consult qualified financial advisor.

Dividend yield mutual funds offer a balanced approach combining equity growth potential with income stability from dividend payouts. This guide explains how they work and their suitability for your portfolio.

Understanding Dividend Yield Mutual Funds

Dividend yield mutual funds invest primarily in dividend-paying stocks. SEBI requires 65% minimum equity allocation. They differ from other equity funds through their income-focused strategy.

What is Dividend Yield?

Dividend Yield = (Annual Dividend per Share ÷ Market Price per Share) × 100

Example: Rs. 10 dividend on Rs. 200 stock = 5% yield. These funds focus on attractive yields relative to stock price, not just absolute dividend amounts.

How Do Dividend Yield Mutual Funds Work?

Stock Selection: Fund managers screen for historical dividend track record, yield vs. benchmark, financial stability, and business fundamentals.

Portfolio: 70-80% in high-dividend-yield stocks; remainder in other equities or cash.

Income Sources:

1. Dividends from portfolio companies

2. Capital appreciation from stock price increases

This dual approach offers both income and growth potential.

Key Features

1. Focus on Established Companies: Invest in mature large-cap/mid-cap companies (banking, FMCG, utilities, pharma) with strong balance sheets.

SIPs can be particularly effective with dividend yield funds, allowing you to build your investment gradually while benefiting from rupee cost averaging.

Dividend Yield Funds vs. Dividend Option

Dividend Yield Fund : A dividend yield fund is a type of equity mutual fund that specifically invests in companies known for paying regular, high dividends – typically blue-chip stocks in sectors like banking, FMCG, utilities, and PSUs. The fund’s strategy focuses on stocks with dividend yields of 3-6%, higher than the market average. These funds aim to generate returns from both the dividends received from portfolio companies AND capital appreciation of stock prices. Examples include ICICI Prudential Dividend Yield Equity Fund and HDFC Dividend Yield Fund.

Dividend Option : The dividend option is a payout structure available in ANY mutual fund (not just dividend yield funds). When you invest in any fund, you can choose between two modes: Growth Option(all returns stay invested and reflected in NAV growth) or Dividend Option (fund periodically pays out profits to you, which reduces NAV proportionally). These payouts are not guaranteed or regular; they’re declared at the fund’s discretion. Importantly, when you receive a dividend payout, it’s essentially your own money being returned to you, not “extra” income.

Performance Considerations

Historically, dividend yield funds underperform growth funds in bull markets but show better resilience during corrections. Over 10+ years, dividends contribute 30-40% of stock returns. Past performance doesn’t guarantee future results.

Building a Balanced Portfolio

Use dividend yield funds as part of diversified strategy:

– Young investors: For stability with growth funds

– Near-retirees: Reduce volatility while keeping equity exposure

Choosing the Right Fund

Consider: track record across cycles, portfolio composition, expense ratio, fund manager experience, and fund size.

If you don’t wish to put in the effort of selecting the funds and would only like to invest for a short period of time to essentially earn some returns on your otherwise lying funds, then parking your money in Curie Money makes so much sense! Curie Money invests the money in liquid funds which can be redeemed almost instantaneously!

Conclusion

Dividend yield funds balance equity growth with dividend-paying stock stability. Suitable for investors prioritizing lower volatility and income with appreciation. Not one-size-fits-all-work best in diversified portfolios aligned with your goals and risk profile.

At Curie Money (AMFI ARN: 257706), we partner with ICICI Prudential and Bajaj Finserv for diverse mutual fund access. Assess your needs and consult a financial advisor for personalized guidance.

Disclaimer:

Mutual fund investments are subject to market risks. Read all scheme documents carefully. Past performance doesn’t indicate future results. Information is educational only, not investment advice. Dividends aren’t guaranteed. Consider your objectives, risk tolerance, and financial situation before investing.

A mutual fund is an investment product, while a SIP is a method of investing in that product. Think of it this way: a mutual fund is like a subscription service, and a SIP is choosing to pay monthly instead of annually.

Understanding Mutual Funds First

A mutual fund is a basket of investments – stocks, bonds, or other assets – professionally managed on your behalf. When you invest, you buy units valued at NAV (Net Asset Value), which fluctuates based on underlying securities’ performance.

Key benefits:

– Professional management by expert fund managers

– Diversification across multiple securities

– Accessible with small amounts

– Variety: equity, debt, hybrid funds for different goals

What Exactly Is a SIP?

A Systematic Investment Plan (SIP) is a disciplined method of investing fixed amounts in mutual funds at regular intervals (monthly, weekly, quarterly) instead of a lump sum. Same fund, different payment approach.

The Core Distinction: Product vs. Method

You cannot choose between a SIP and a mutual fund – they’re not competing options. When you “invest in a SIP,” you’re investing in a mutual fund through the SIP method.

Two Ways to Invest in Mutual Funds

The Lump Sum Approach

Invest the entire amount at once (e.g., Rs 2 lakh bonus).

Makes sense when: You have money available, market conditions look favorable, comfortable with timing.

Watch out for: Entire investment exposed to market at one point; timing the market is difficult.

The SIP Approach

Invest the same amount over time (e.g., Rs 16,667 monthly for 12 months).

Makes sense when: You have regular income, want to avoid timing stress, prefer gradual wealth building.

Watch out for: In rising markets, lump sum may give better returns; requires discipline.

The better approach!

Another approach of getting exposure in mutual funds by keeping money in your Curie Money account. Whatever funds are available in your account, Curie Money invests this amount smartly in various liquid funds, essentially enabling you to enjoy mutual funds returns on money that would otherwise have been simply parked in a savings account. As and when you need the funds, Curie Money liquidates the investment to provide instantaneous liquidity!

Key Differences at a Glance

Aspect

Mutual Fund (as a product)

SIP (as a method)

Nature

Investment product/scheme

Method of investing in mutual funds

Investment Mode

Can be lump sum or SIP

Regular, fixed amounts invested periodically

Flexibility

Depends on the type of fund (some can be more flexible)

High – can start, stop, or modify anytime

Market Timing

Relevant for lump sum investment timing

Less critical due to rupee cost averaging

Discipline

Requires one-time decision

Builds investment discipline naturally over time

Minimum Amount

Varies by fund (often Rs 5,000+ for lump sum)

Typically low, starting from Rs 500 for most funds

The Power of Rupee Cost Averaging

SIPs offer rupee cost averaging: your fixed amount buys more units when markets are down, fewer when up. This can lower your average cost per unit over time. Note: This reduces timing risk but doesn’t guarantee profits. You can also enjoy the benefit if rupee cost averaging with the help of Curie Money, where your investments are automated!

Building Investment Discipline

SIPs automate savings – Rs 5,000 auto-debited monthly forces you to adjust spending and prioritize financial goals, unlike lump sum where spending temptation is higher.

Which Approach Should You Choose?

The answer isn’t about choosing SIP or mutual fund (since SIP is a way to invest in mutual funds), but rather: should you invest via SIP or lump sum?

Consider SIP if you:

– Have regular monthly income

– Are new to mutual fund investing

– Want to reduce the stress of market timing

– Prefer gradual wealth accumulation

– Have long-term financial goals

Consider Lump Sum if you:

– Have received a windfall (bonus, inheritance, maturity proceeds)

– Have thoroughly researched and believe markets are attractively valued

– Are comfortable with short-term volatility

– Have investment experience

The middle ground: Many smart investors use both. They invest monthly SIPs for regular savings while also making lump sum investments when they have extra cash available.

Or if you’d like your idle money to earn you returns via mutual funds investment while not sacrificing liquidity, then you can go ahead with Curie Money!

Curie Money offers instant mutual funds investment of your idle funds. These funds are invested in liquid funds which means that when you require your money, the equivalent amount is liquidated, providing you with instant liquidity!

Common Misconceptions Clarified

Myth 1: “SIPs are safer than mutual funds”

Reality: SIPs are a method – risk depends on the fund type chosen.

Myth 2: “SIPs guarantee returns”

Reality: No guarantees. Returns depend on market performance.

Myth 3: “SIPs can’t lose money”

Reality: Poor market/fund performance can still cause losses.

Myth 4: “Lump sum is only for the rich”

Reality: It just means investing available money at once, not about wealth.

How to Start Your Mutual Fund Investment Journey

Whether you choose SIP or lump sum, here’s what you need to do:

1. Complete KYC: This one-time Know Your Customer verification is mandatory

2. Identify Your Goals: Are you investing for retirement, a child’s education, or wealth creation?

3. Assess Risk Appetite: Can you handle market volatility, or do you prefer stability?

4. Choose Appropriate Funds: Equity for long-term growth, debt for stability, hybrid for balance

5. Decide Investment Method: SIP for regular investing, lump sum when you have cash available

6. Monitor and Review: Check your investments periodically but avoid obsessive tracking

Final Thoughts

SIPs and mutual funds aren’t competing products. A mutual fund is what you invest in; SIP is how you invest. Choose the method (SIP, lump sum, or both) based on your financial situation and goals. What matters most: choosing quality funds, maintaining discipline, and giving investments time to grow.

Mutual fund investments are subject to market risks. Read all scheme-related documents carefully. Past performance is not indicative of future results.

Whether you choose SIP or lump sum investment, platforms like Curie Money make it seamless with instant UPI access to your mutual fund investments. Powered by ICICI Prudential and Bajaj Finserv liquid funds, with YES Bank as the banking partner. (AMFI ARN: 257706)

Disclaimer:

Mutual fund investments are subject to market risks. Read all scheme documents carefully. Past performance doesn’t indicate future results. Information is educational only, not investment advice. Dividends aren’t guaranteed. Consider your objectives, risk tolerance, and financial situation before investing.

When building a diversified investment portfolio in India, Exchange-Traded Funds (ETFs) and Mutual Funds are two popular options. While both allow you to invest in a basket of securities, they differ significantly in structure, costs, and how they’re traded. This guide explains the key differences to help you choose the right option

What Are Mutual Funds?

A mutual fund pools money from multiple investors and invests it across various securities—stocks, bonds, or both. Professional fund managers actively research companies, select securities, and adjust portfolios to meet the fund’s investment objective. When you invest in a mutual fund, your transaction is processed at the end-of-day Net Asset Value (NAV), which is calculated after market hours. You don’t need a demat account, and you can set up systematic investment plans (SIPs) with automated monthly debits from your bank account.

What Are Exchange-Traded Funds (ETFs)?

ETFs are investment funds that trade on stock exchanges like individual company shares. Most ETFs follow a passive investment approach, tracking a market index such as Nifty 50 or BSE Sensex. The ETF holds the same stocks in the same proportion as the index, aiming to replicate its performance. You need a demat and trading account to invest in ETFs. Unlike mutual funds, ETF prices fluctuate in real-time throughout trading hours, allowing you to buy or sell at any moment during market sessions. This provides intraday trading flexibility but also means you need to actively place buy/sell orders.

ETFs vs Mutual Funds: Complete Comparison

Feature

ETFs

Mutual Funds

Trading

Real-time on stock exchanges

Once daily at end-of-day NAV

Price Discovery

Market price (supply/demand)

NAV calculated after market close

Management Style

Mostly passive (index-tracking)

Active or passive

Expense Ratio

0.05-0.50% annually

0.50-2.50% annually

Minimum Investment

1 unit (~₹100-₹5,000)

SIP: ₹500+, Lumpsum: ₹5,000+

Demat Account

Required

Not required

SIP Automation

Manual (platform-dependent)

Built-in, automated

Brokerage Charges

Yes (₹10-20 per trade)

No

Exit Load

No, but brokerage applies

0-1% (if redeemed early)

Transparency

Real-time holdings visible

Monthly disclosure (1-month lag)

Liquidity

Depends on trading volume

High (direct redemption from AMC)

Fractional Units

No

Yes

Best For

Cost-conscious, passive investors

SIP investors, active strategies

Key Differences Explained

1. Trading and Liquidity

ETFs trade continuously during market hours (9:15 AM to 3:30 PM) at real-time market prices determined by supply and demand. You can buy during a market dip at 11 AM or sell during a rally at 2 PM. However, liquidity depends on trading volumes—low-volume ETFs may have wider bid-ask spreads, increasing your transaction costs.

Mutual Funds transact once daily at the NAV calculated after market closes. If you place a purchase order at 10 AM, you’ll get units at that day’s closing NAV (calculated around 9-10 PM). This means you don’t know the exact price when placing your order. Redemptions are processed within 1-3 business days directly with the AMC, ensuring liquidity regardless of market trading volumes.

2. Management Style

ETFs predominantly follow a passive approach, mechanically replicating an index. If Nifty 50 contains 50 stocks, the ETF holds the same 50 stocks in identical proportions. There’s minimal human intervention—no active buying/selling based on market views. This simplicity keeps costs low.

Mutual Funds can be actively managed (fund managers make active buy/sell decisions to beat the index) or passively managed (index funds that track indices like ETFs but are structured as mutual funds). Actively managed funds aim to outperform benchmarks through research, stock selection, and tactical allocation—though 70-80% underperform their benchmarks over 10+ years.

3. Understanding Tracking Error (ETFs)

While ETFs aim to replicate index returns, they don’t achieve perfect replication due to:

– Expense ratios deducted from returns

– Rebalancing costs when index composition changes

– Cash drag from dividend holdings

– Transaction costs

Example:

– Nifty 50 Index returns: 15% annually

– Nifty 50 ETF returns: 14.80% annually

– Tracking error: 0.20%

Look for ETFs with tracking errors below 0.25% for efficient index replication. Lower tracking error indicates better fund management quality.

4. NAV vs Market Price (ETFs)

Net Asset Value (NAV): The actual value of the ETF’s underlying holdings divided by total units. Calculated based on closing prices of all securities in the portfolio.

Market Price: The price at which the ETF trades on the exchange, determined by buyer-seller demand.

Example:

– ETF NAV at 3:30 PM: ₹100.00

– ETF market price: ₹100.40 (trading at 0.4% premium)

– OR: ₹99.80 (trading at 0.2% discount)

Why they differ: Supply-demand imbalances, liquidity constraints, or market timing differences. High-volume ETFs typically trade very close to NAV (within 0.1-0.3%), while low-volume ETFs may have wider gaps.

5. True Cost Comparison

Beyond expense ratios, consider the total cost of ownership:

ETF Real Costs (₹1 lakh invested for 5 years):

– Expense ratio: 0.15% annually = ₹750 total

– Brokerage (buy + sell): ₹40

– Securities Transaction Tax (STT): ~₹100

– Impact cost (bid-ask spread): ₹50

– Total cost: ~₹940

Mutual Fund Direct Plan (₹1 lakh for 5 years):

– Expense ratio: 1% annually = ₹5,000 total

– No brokerage/STT

– Exit load: ₹0 (if held >1 year)

– Total cost: ~₹5,000

Mutual Fund Regular Plan (₹1 lakh for 5 years):

– Expense ratio: 2% annually = ₹10,000 total

– Total cost: ~₹10,000

Cost savings: ETF saves ₹4,060 vs. direct mutual fund, ₹9,060 vs. regular mutual fund over 5 years. Over 20 years with compounding, this difference becomes ₹50,000-₹1,00,000+ on a ₹1 lakh investment.

Tax Treatment (FY 2024-25)

Equity ETFs and Equity Mutual Funds

Tax treatment is identical:

Long-Term Capital Gains (holding >12 months):

– Tax rate: 12.5%

– Annual exemption: ₹1.25 lakh (cumulative across all equity investments)

Short-Term Capital Gains (holding ≤12 months):

– Tax rate: 20%

Debt ETFs and Debt Mutual Funds

For investments made on/after April 1, 2023:

– All gains taxed at your income tax slab rate (any holding period)

– No LTCG benefit

For investments made before April 1, 2023:

– Complex grandfathering rules apply based on sale date

– See our detailed LTCG tax article for specifics

Key Point: Tax treatment is identical between ETFs and mutual funds within the same category (equity/debt).

Which Should You Choose?

Choose ETFs if you:

– Prefer low-cost, passive investing focused on index returns

– Have a lumpsum amount to invest (not regular monthly investments)

– Want real-time trading flexibility during market hours

– Are comfortable managing your own portfolio actively

– Already have a demat account or don’t mind opening one

– Believe in buy-and-hold with minimal transactions

– Want complete transparency of holdings

Choose Mutual Funds if you:

– Value professional fund management and research

– Invest through monthly SIPs (₹5,000-₹20,000)

– Seek diversification across multiple asset classes

– Want automated investment without manual intervention

– Prefer not to maintain a demat account

– Need systematic withdrawal plans (SWP) for regular income

– Want access to actively managed strategies in less efficient market segments

Alternate to Manual investing in Mutual Funds:

Companies like Curie Money enable the investors to seamlessly invest in mutual funds without taking any effort. All that the investor needs to do is park their money (as they do in their bank account) in Curie Money. And Curie Money will invest on the investor’s behalf in liquid mutual funds. The silver lining is that the funds are always readily available, i.e. as and when you make a debit, your equivalent investment is liquidated instantaneously! This is highly convenient for individuals who wish to enjoy returns in every penny that too without the hassle of researxhing good mutual funds!

Practical Considerations

ETF Challenges:

– Requires monitoring bid-ask spreads before trading

– Low-volume ETFs may have poor liquidity

– Manual SIP setup (not auto-debit)

– Demat account annual maintenance (₹300-500)

– Brokerage costs on each transaction

– Need to place orders during market hours

Mutual Fund Advantages:

– Seamless SIP automation with bank mandate

– Can invest exact amounts (e.g., ₹7,543)

– Fractional units allowed

– Direct redemption with AMC (no market dependency)

– Free portfolio rebalancing (switches between schemes)

– Systematic Transfer Plans (STP) and Withdrawal Plans (SWP)

Combining Both Strategically

Many sophisticated investors use both:

Core holdings: ETFs for large-cap exposure (60-70% of equity)

Satellite positions: Active mutual funds for mid/small-cap opportunities (20-30%)

Debt allocation: Mutual funds for ease of SWP in retirement

This approach maximizes cost efficiency while retaining flexibility where active management can add value.

Another approach is to park your funds with Curie money, and enjoy mutual fund investment without taking any effort of selection and investment. As and when you need your funds, equivalent investment is liquidated!

Important Considerations

Both ETFs and mutual funds carry market risks. Equity investments can be volatile in the short term. Past performance doesn’t guarantee future results. Assess your financial goals, risk tolerance, investment horizon, and comfort with different investment mechanisms before choosing. Neither option is inherently superior—the right choice depends on your specific situation, investment behavior, and preferences.

Conclusion

ETFs offer ultra-low costs, transparency, and real-time trading flexibility, making them ideal for cost-conscious passive investors with lumpsum investments. Mutual funds provide professional management, seamless SIP automation, and convenience without needing a demat account, suiting systematic investors and those seeking active strategies.

The best approach for many investors is using both strategically—ETFs for core index exposure and mutual funds where active management or systematic investing adds value. Focus on your investment goals and behavior patterns rather than searching for a universally better option.

Curie Money (AMFI ARN: 257706) partners with ICICI Prudential and Bajaj Finserv to offer access to quality mutual funds investment options. Choose based on your needs, or strategically combine both.

Disclaimers:

Mutual fund and ETF investments are subject to market risks. Read all scheme-related documents carefully before investing. Past performance is not indicative of future results. This information is for educational purposes only, not investment advice. Consider your financial goals and risk tolerance before making investment decisions.

When it comes to investing, many people immediately think of stocks and equities. However, debt funds offer another avenue worth exploring for those looking to grow savings while maintaining a conservative approach to risk.

What is a Debt Fund?

A debt fund is a type of mutual fund that invests in fixed-income securities like government bonds, corporate bonds, treasury bills, and commercial papers. Unlike equity funds that invest in stocks, debt funds focus on instruments that typically offer more predictable returns through regular interest payments.

When you invest in a debt fund, the fund manager pools your money with other investors and invests in various debt instruments with pre-decided maturity dates and interest rates. While debt funds are among the lower-risk mutual fund categories, they’re subject to market risks and do not offer guaranteed returns.

How Do Debt Funds Work?

Fund managers select quality instruments based on credit ratings (AAA, AA, etc.) from agencies like CRISIL, ICRA, or CARE. They manage interest rate risk by adjusting portfolio duration, as bond prices and interest rates move inversely.

Debt funds generate returns through interest income and capital appreciation when bond values rise. The NAV fluctuates based on interest rates and credit quality, making returns market-linked and not guaranteed.

Types of Debt Funds

By Duration:

– Liquid Funds: 91-day maturity, high liquidity, suitable for short-term parking

– Dynamic Bond Funds: Flexible maturity based on interest rate outlook

Who Should Invest in Debt Funds?

– Conservative investors with lower risk appetite prioritizing capital preservation

– Short to medium-term investors saving for goals from a few months to several years

– Income seekers looking for regular income streams

– Portfolio diversifiers wanting to reduce overall volatility

– First-time investors starting with lower-risk mutual fund options

Benefits of Investing in Debt Funds

1. More Stable Returns: Less volatile than equity funds with relatively predictable income streams

2. Professional Management: Expert fund managers monitor credit quality and interest rate trends

3. High Liquidity: Quick redemptions, typically within 1-2 business days for liquid funds

4. Diversification: Spread across multiple instruments and issuers

5. Market Access: Access to wholesale instruments like commercial papers and corporate bonds

6. Flexible Options: Categories for various investment horizons

7. Potential Tax Benefits: Indexation benefits on long-term gains

Risks Associated with Debt Funds

1. Credit Risk: Issuer may default on payments; ratings can change

2. Interest Rate Risk: Bond values fall when interest rates rise; long-duration funds are more sensitive

3. Liquidity Risk: Difficulty selling securities quickly in certain market conditions

4. Reinvestment Risk: Lower returns when reinvesting at reduced interest rates

5. Market Risk: Economic factors and regulatory changes impact performance

Important: Debt funds carry market risks and don’t offer guaranteed returns. They’re not covered by DICGC insurance like bank deposits.

Taxation on Debt Funds

– Short-Term (< 3 years): Added to income, taxed at your slab rate

– Long-Term (> 3 years): 20% tax with indexation benefits

Tax laws are subject to change. Consult a tax professional for personalized advice.

How to Choose the Right Debt Fund

1. Match Investment Horizon: Align fund duration with your financial goals

2. Assess Risk Tolerance: Choose between safer gilt/corporate bond funds or higher-return credit risk funds

3. Check Credit Quality: Prefer AAA/AA-rated securities for lower risk

4. Review Expense Ratio: Lower fees significantly impact net returns

5. Evaluate Performance: Compare with similar funds and benchmarks

6. Understand Strategy: Review investment approach and portfolio duration

7. Check Fund Manager Track Record: Experience matters in debt management

The alternate method!

A smart alternative to putting efforts and manually choosing the fund is to simply invest with Curie Money! All you have to do is just park your money like you do with a savings account. Curie Money smartly invests your money in liquid funds, which are liquidated instantaneously as and when you need funds. This essentially means that you earn returns on the money without the hassle of going through the selection and investment process!

Frequently Asked Questions

Are debt funds safe?

Debt funds are lower-risk but not risk-free. They carry credit, interest rate, and market risks. Unlike FDs, they’re not covered by deposit insurance.

How are they different from fixed deposits?

– Returns: Market-linked (debt funds) vs. predetermined (FDs)

– Liquidity: Higher without penalties vs. early withdrawal charges

– Risk: Market risks vs. DICGC insurance (up to ₹5 lakh)

– Taxation: Indexation benefits vs. slab-rate taxation

Can I withdraw anytime?

Yes, most debt funds offer high liquidity with redemptions in 1-3 business days. Some may have exit loads for early withdrawals. This liquidity can also be enjoyed with Curie Money! As and when you need funds, your investment of equivalent value is liquidated instantaneously, providing your with unmatched convenience!

What returns can I expect?

Returns vary by category and market conditions. Liquid funds offer moderate returns, while longer-duration funds may provide higher returns with more volatility. Returns are not guaranteed.

Which is suitable for beginners?

Liquid or ultra-short duration funds with high-quality securities offer relatively stable returns and high liquidity for first-time investors.

Conclusion

Debt funds offer exposure to fixed-income securities with professional management for various investment goals. While they’re lower-risk than equity funds, they carry market risks and don’t offer guaranteed returns or deposit insurance coverage.

When choosing a debt fund, consider your investment horizon, risk tolerance, portfolio quality, expense ratio, and performance. Ensure alignment with your overall financial plan.

For those seeking better returns on savings with instant UPI access, Curie Money offers investment-linked payment solutions. It invests in SEBI-regulated liquid funds managed by ICICI Prudential and Bajaj Finserv Asset Management, combining potential for better returns with instant accessibility for daily transactions.

—

Disclaimers

Mutual fund investments are subject to market risks. Read all scheme-related documents carefully. Past performance is not indicative of future results.

Debt funds don’t offer guaranteed returns. Returns are market-linked and vary based on interest rates, credit quality, and market conditions. This information is for educational purposes only, not investment advice.

Debt funds carry credit, interest rate, liquidity, and market risks. They’re not bank deposits and lack DICGC insurance coverage. Tax laws may change; consult a tax professional.

Assess your investment objectives, risk tolerance, and financial situation before investing. Consider consulting a qualified financial advisor.

About Curie Money: India’s first UPI app that grows your money. Funds invested in liquid mutual funds managed by ICICI Prudential and Bajaj Finserv Asset Management. Banking via YES Bank. AMFI-registered distributor (ARN: 257706). NPCI-approved, PCI-DSS compliant, SEBI-regulated. Returns are market-linked, not guaranteed.